DATASET

Dataset Profile

A structured examination of dataset depth, coverage, and statistical properties across 80+ days of continuous collection.

01 Dataset at a Glance

02 Anatomy of a Single Row

row ─────────────────────────────────────────────────────────

│

├── symbol (string)

├── snapshot_ts (ISO 8601)

│

├── meta ─────────────────────────────────── 22 fields

│ ├── session_id (UUID v4)

│ ├── schema_version, scoring_version

│ ├── duration_sec, sample_count, total_samples

│ ├── universe tracking (page, snapshot_id, lag)

│ └── lifecycle timestamps (added, expires, expired)

│

├── spot_raw ─────────────────────────────── 19 fields

│ ├── mid, bid, ask, last, spread_bps

│ ├── range_pct_24h, ticker24_chg

│ ├── taker_buy_ratio_5m, obi_5

│ ├── depth_5bps_quote, depth_10bps_quote, depth_25bps_quote

│ ├── depth_bid_qty_quote, depth_ask_qty_quote

│ ├── micro_premium_pct, avg_impact_pct

│ └── spread_eff_raw, liq_eff_raw, liq_qv_usd

│

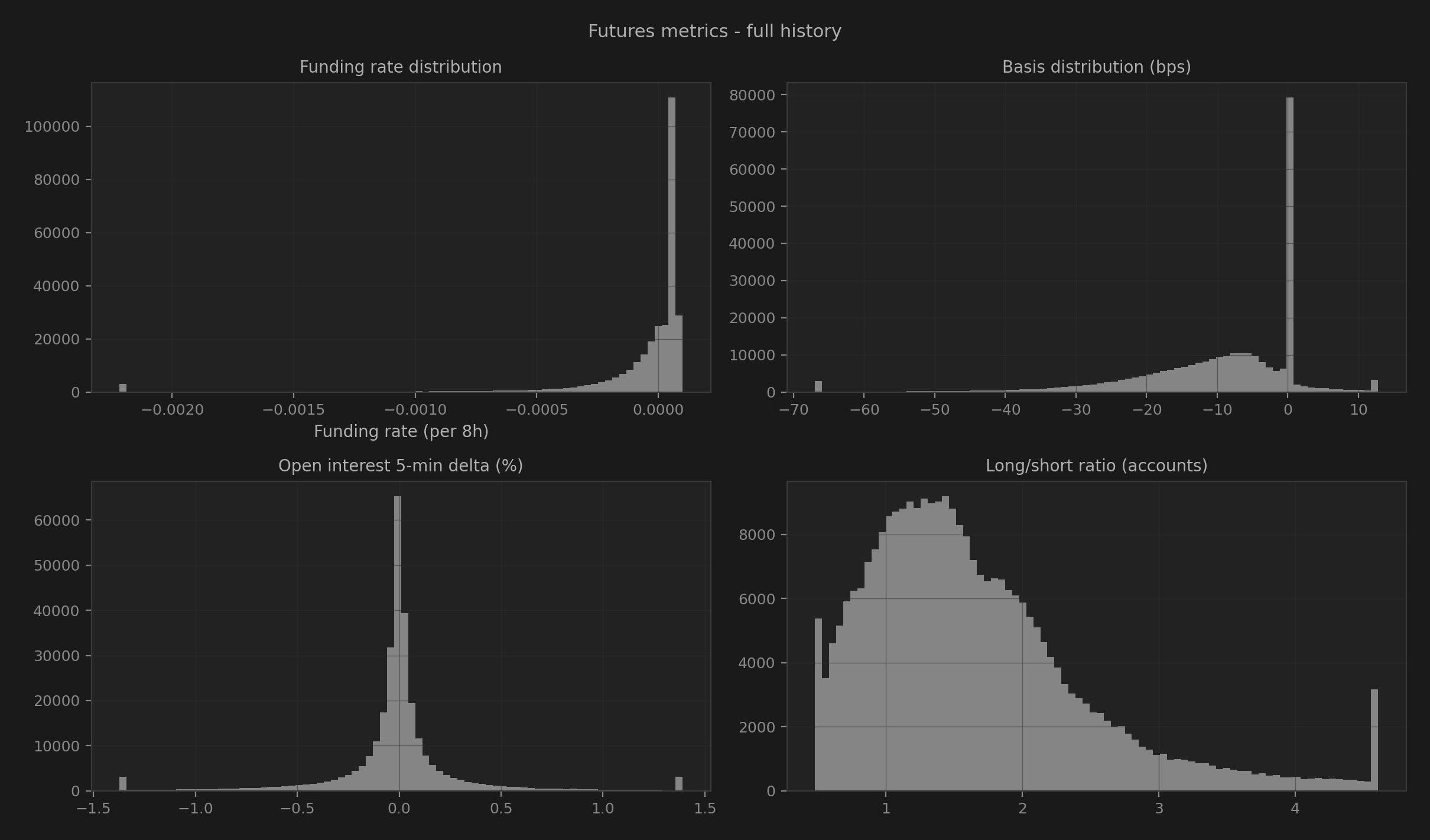

├── futures_raw ──────────────────────────── 10 fields

│ ├── contract, last_updated_ts, age_sec

│ ├── funding_now, funding_24h_mean

│ ├── open_interest, open_interest_5m_delta_pct

│ ├── basis_now_bps

│ └── top_long_short_accounts_5m, top_long_short_positions_5m

│

├── derived ──────────────────────────────── 9 fields

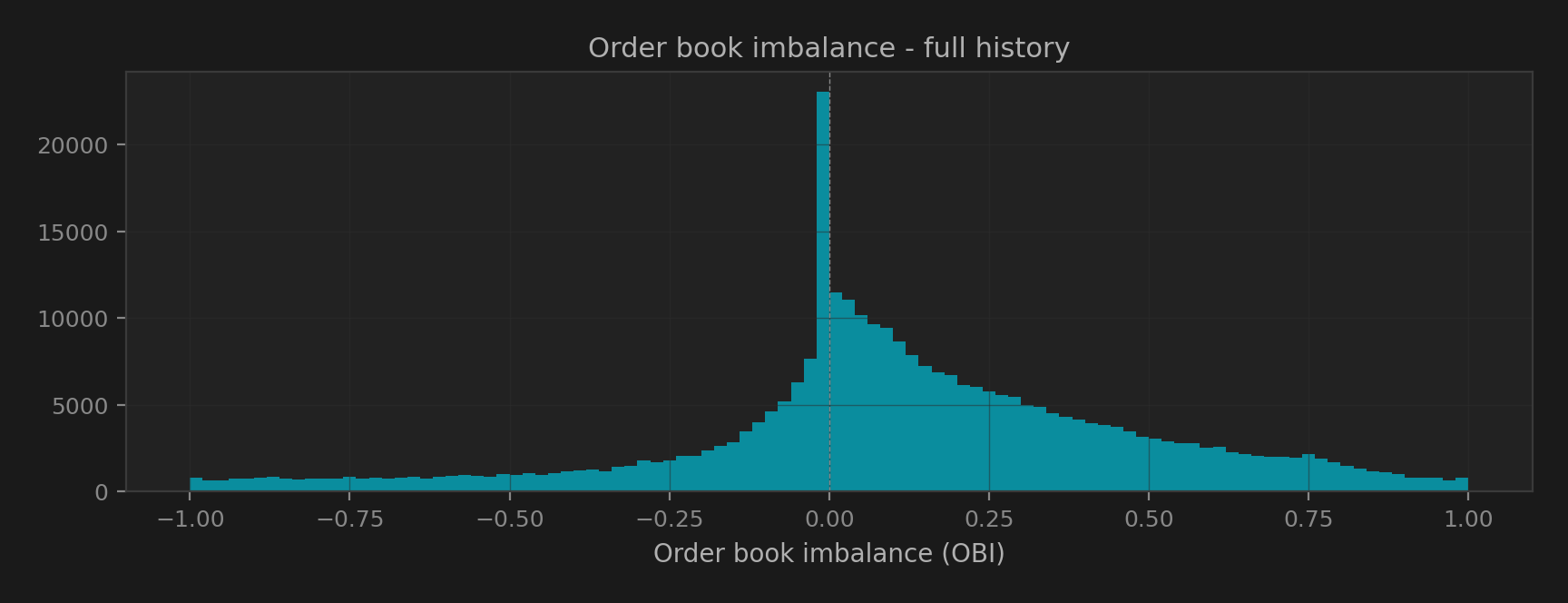

│ ├── depth_spread_bps, depth_weighted, depth_imbalance, depth_skew

│ ├── flow (0–100)

│ ├── liq_global_pct, liq_self_pct

│ └── spread_pct, spread_bps

│

├── scores ───────────────────────────────── 13 factors

│ ├── final (composite)

│ ├── mom, vol, str, liq, spread, taker, flow, depth, microstruct

│ └── spread_eff_score, liq_eff_score, compression_score

│

├── flags ────────────────────────────────── 12 fields

│ ├── spot_data_ok, futures_data_ok, twitter_data_ok

│ ├── futures_stale, futures_contract_exists

│ ├── mom_fallback, vol_fallback, spread_fallback

│ └── compression_enabled, pair_bonus_applied (float)

│

├── twitter_sentiment_windows

│ ├── last_cycle ───────────────────────── ~50 fields

│ │ ├── posts_total, posts_pos, posts_neu, posts_neg

│ │ ├── lexicon_sentiment → {scale, score}

│ │ ├── category_counts → {positive_general, negative_general,

│ │ │ pump_hype, fud_fear, meme_slang,

│ │ │ scam_rug, emoji_pos, emoji_neg}

│ │ ├── top_terms → {6 arrays of top-3 terms per category}

│ │ ├── platform_engagement → {likes, retweets, replies,

│ │ │ quotes, bookmarks, impressions}

│ │ ├── author_stats → {distinct_total, distinct_blue,

│ │ │ distinct_verified, followers_sum/

│ │ │ mean/median/max}

│ │ ├── content_stats → {original, retweets, with_cashtags,

│ │ │ with_hashtags, with_links,

│ │ │ with_media, with_mentions}

│ │ ├── ai_sentiment → {scoring_system, primary_model,

│ │ │ referee_model, posts_scored,

│ │ │ prob_mean/std/min/max,

│ │ │ label_3class_mean}

│ │ ├── hybrid_decision_stats

│ │ │ ├── posts_scored, posts_pos/neu/neg

│ │ │ ├── mean_score, pos/neg/neu_ratio

│ │ │ ├── primary_conf_mean, referee_conf_mean

│ │ │ └── decision_sources

│ │ │ ├── single_model (count)

│ │ │ ├── primary_default (count)

│ │ │ ├── referee_override (count)

│ │ │ └── referee_neutral_band (count)

│ │ └── sentiment_activity → {recent_posts_count,

│ │ has_recent_activity, is_silent,

│ │ latest_tweet_at, hours_since_latest_tweet}

│ │

│ └── last_2_cycles ───────────────────── same structure

│ (aggregated with SUM/AVG/MAX/MERGE semantics)

│

├── twitter_sentiment_meta ───────────────── 15 fields

│ ├── source, captured_at_utc, key_used

│ ├── cycle_id, cycle_start_utc, cycle_end_utc

│ ├── scraper_version, sentiment_model_version, lexicon_version

│ ├── is_silent, methodology_regime (v1/v2)

│ └── bucket_meta (platform, coin, date, span)

│

├── spot_prices ──────────────────────────── 700+ samples

│ └── [{ts, mid, bid, ask, spread_bps}, ...]

│ 10-second intervals across full 2-hour session

│

└── diag ─────────────────────────────────── 4 fields

├── builder_version, build_duration_ms

└── admission_validated, admission_validation_ts

03 The Price Array

. Enables microstructure regime detection.")

04 Sentiment Architecture

X (Twitter) posts

→ asset-specific query filtering

→ deduplication (each post scored once)

→ crypto relevance classifier (off-topic removal)

→ BERTweet primary scoring

→ confidence threshold check

→ HIGH confidence → accept primary label

→ LOW confidence → DistilBERT referee

→ agree → accept

→ disagree → referee overrides

→ uncertainty band → force neutral

→ cycle-level aggregation

→ dual time window output (last_cycle + last_2_cycles)

.")

Methodology upgrade (Phase 1 cutover: 2026-02-16T05:14:00Z): The visible shift in decision source ratios beginning February 17 reflects a phased transition to the V2 pipeline. Primary sentiment model upgraded to an improved DistilBERT variant (approximately 50% better negative-sentiment detection on crypto-labeled training data), and the referee model upgraded to a BERTweet-based architecture with better-calibrated confidence scoring. Crypto relevance filtering was activated in Phase 2 at 2026-02-17T06:03:00Z. Data produced under each methodology is marked in methodology_regime ("v1" or "v2").

.")

Hybrid dual-model architecture explained: Every sentiment prediction audit trail records which decision rule fired (decision_source). Primary default = highest-accuracy model working independently. Referee override = second model (optimized for calibration) strongly disagreed (≥0.90 confidence). Referee neutral = second model flagged ambiguity (confidence band 0.40-0.60), forcing neutral score. Reporting includes aggregates over last_cycle (most recent full query cycle, ~50-60 minutes) and last_2_cycles (aggregation of the last two query cycles).

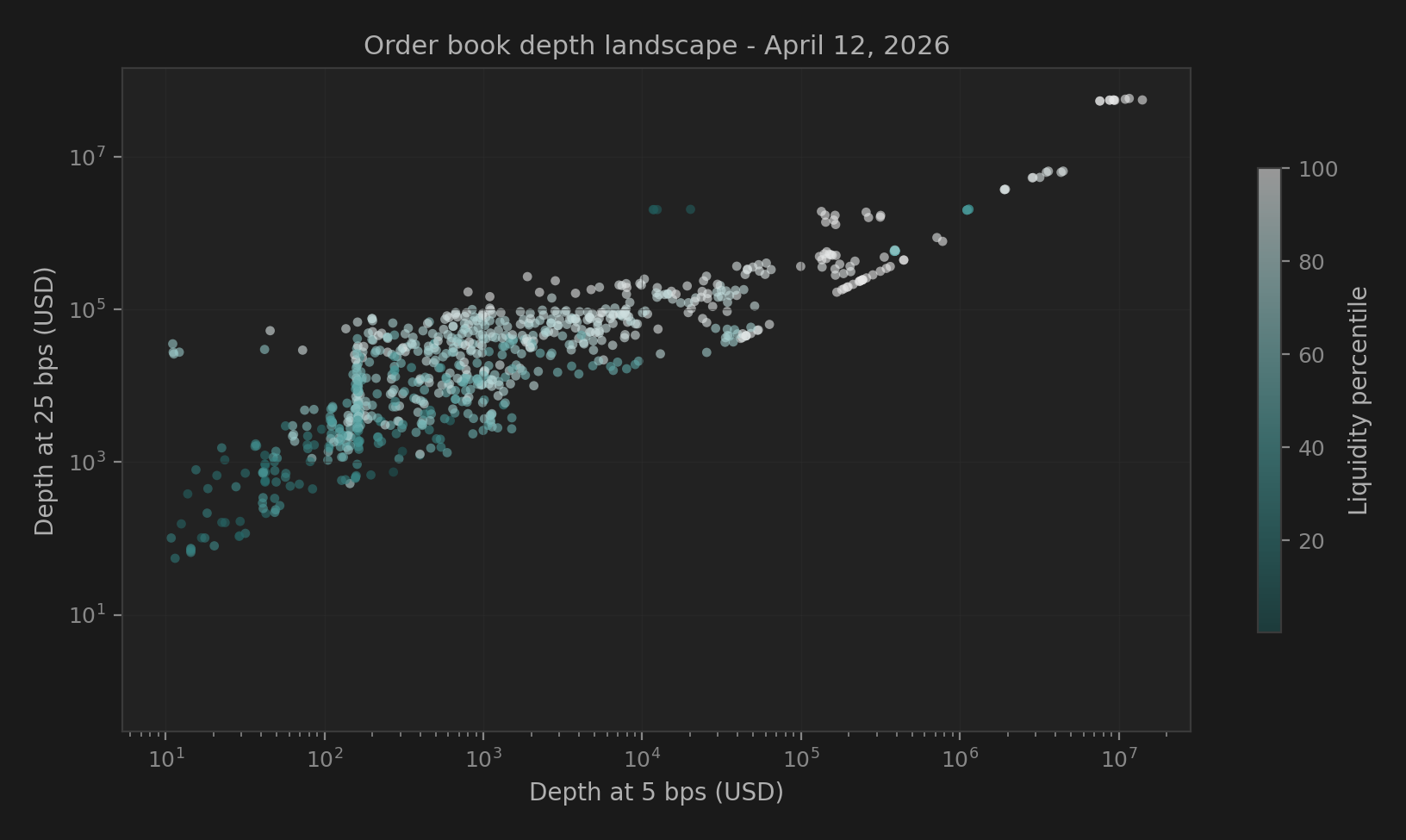

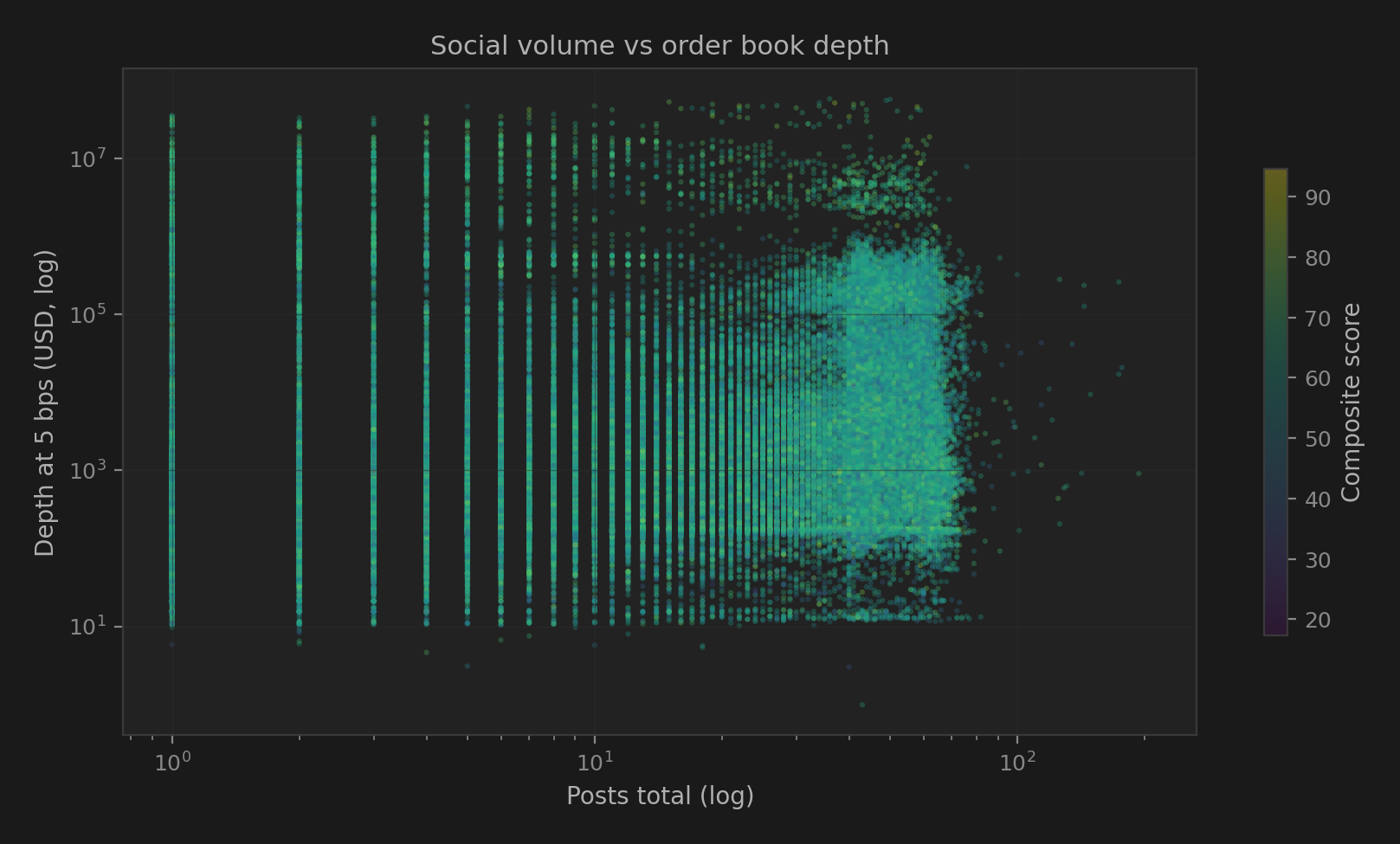

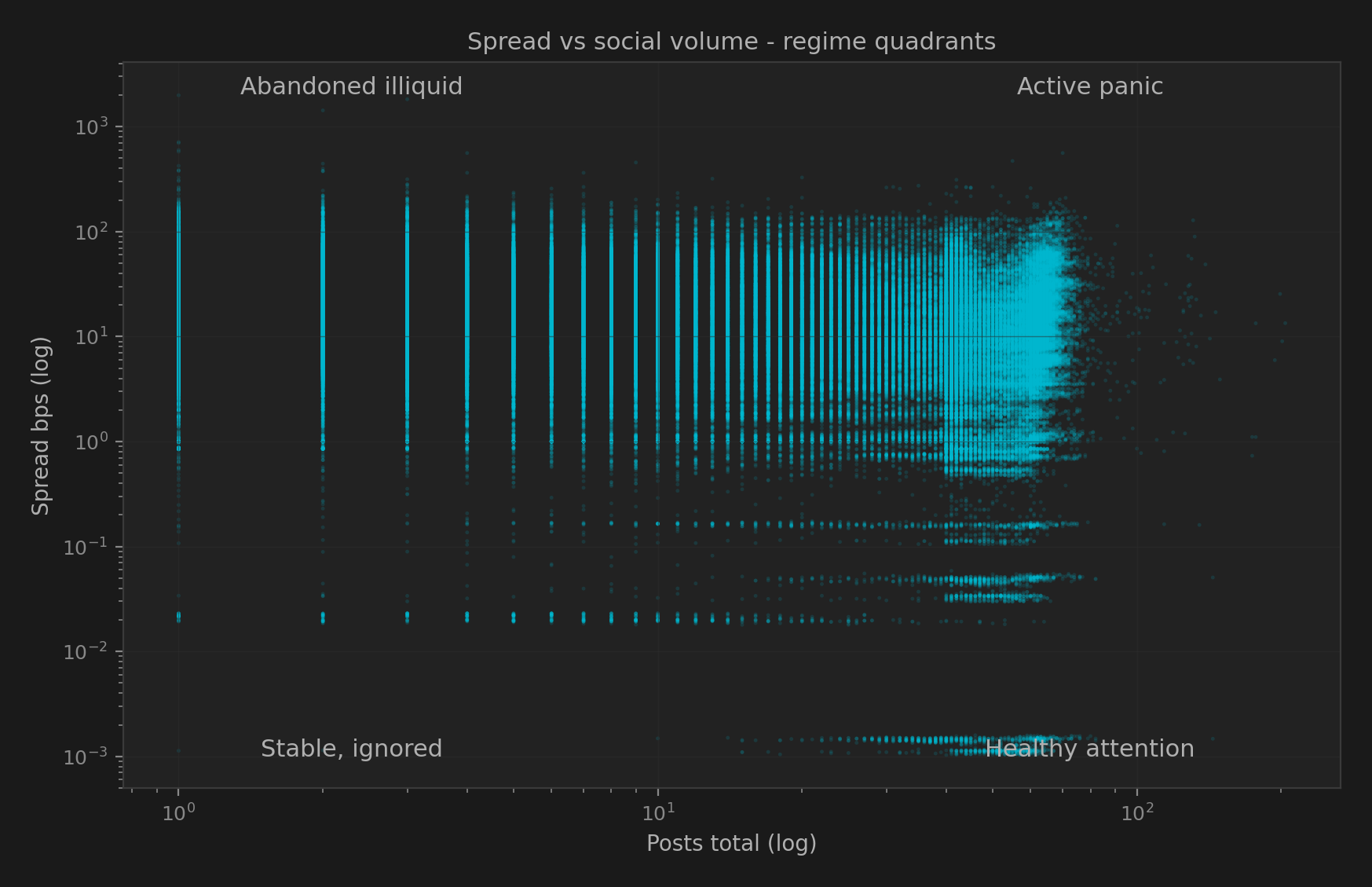

05 Market Microstructure

06 Cross-Domain Analysis

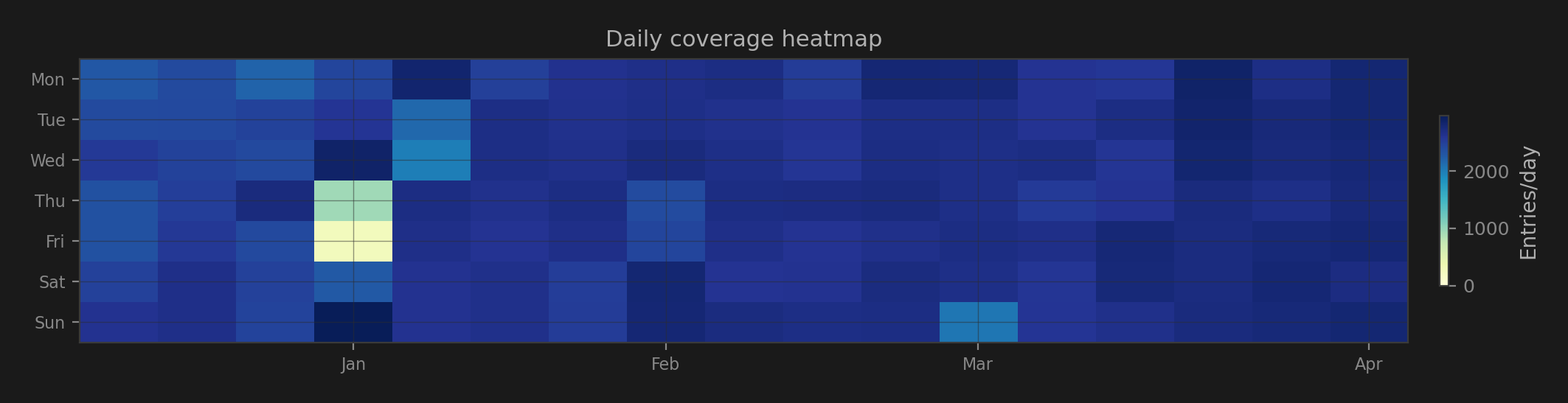

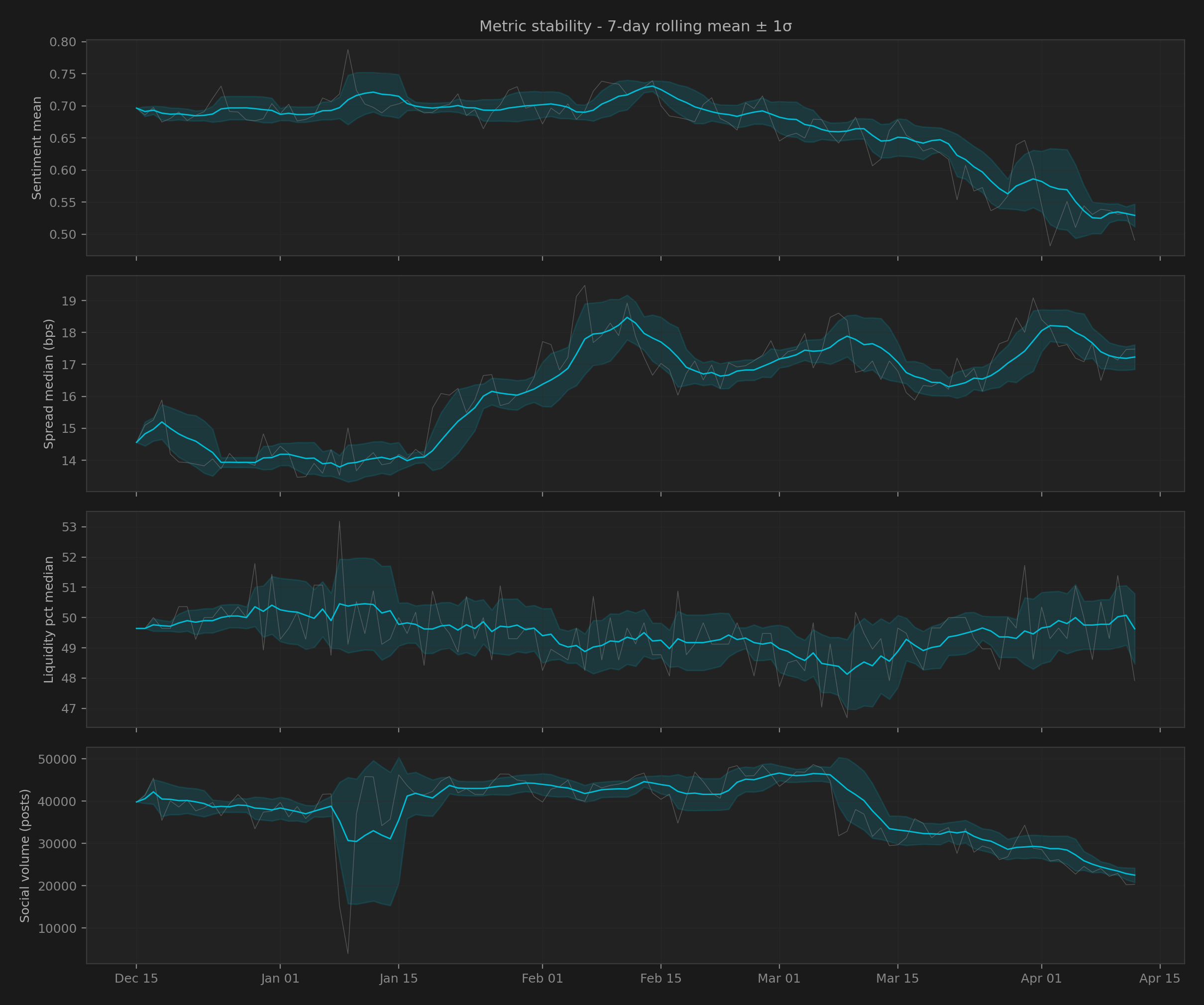

07 Temporal Consistency

Data collection event (January 8-9): Collection volume dropped on January 8-9 during infrastructure migration of the data pipeline to a new server. Normal collection resumed January 10. Futures data for early archive entries was backfilled on January 15 using Binance's 30-day historical archive; affected rows carry futures_stale: false following the backfill.

The sentiment pipeline was upgraded from V1 (single-model DistilBERT) to V2 (dual-model BERTweet + DistilBERT referee with crypto relevance filter) in February 2026. Each row carries a methodology_regime field ("v1" or "v2") for programmatic separation.

08 Tail Behavior & Stress Capture

The following observations document the range of conditions captured in the archive - from illiquid micro-caps to high-volume events - confirming the pipeline operates across the full distribution of market states.

| Category | Asset | Date | Value |

|---|---|---|---|

| Highest social volume | JUP | 2026-03-30 | 204.00 posts |

| Widest spread | DF | 2026-02-07 | 1,992 bps |

| Largest OI delta | DOLO | 2026-01-12 | 114.04 % |

| Most extreme funding | ONT | 2025-12-27 | -0.020000 per 8h |

| Highest compression | AAVE | 2025-12-15 | 50.00 score |

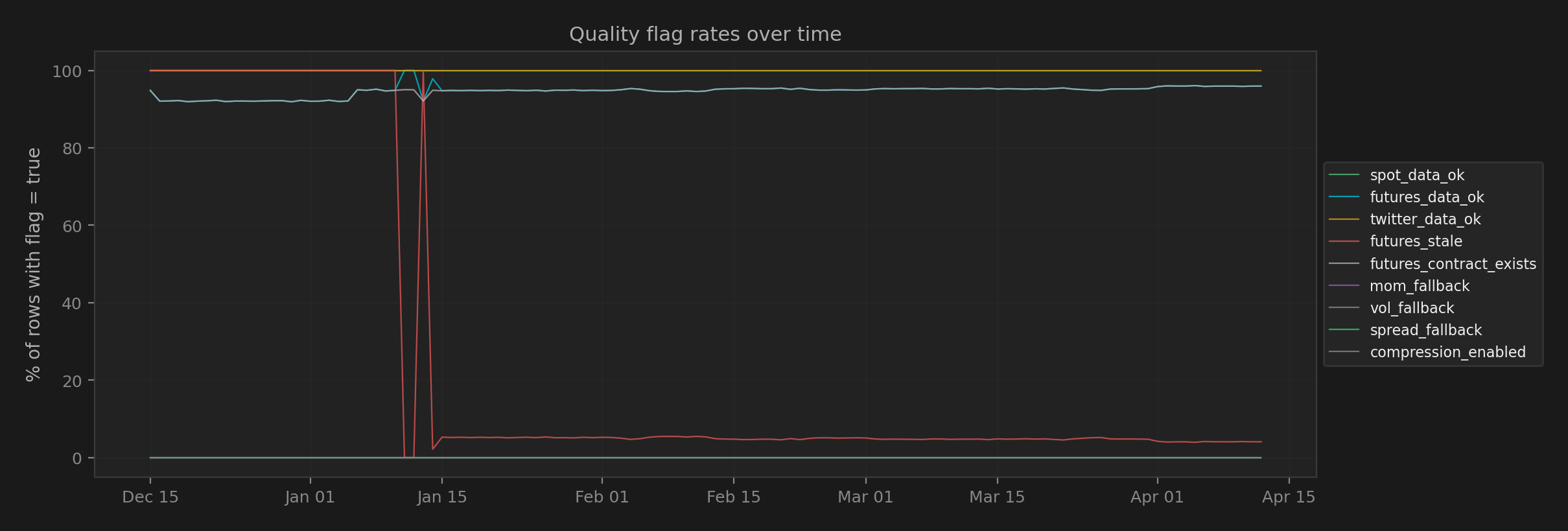

09 Data Quality Framework

| Flag | Type | What it indicates |

|---|---|---|

spot_data_ok | bool | Spot market data captured successfully |

futures_data_ok | bool | Futures data captured successfully |

twitter_data_ok | bool | Sentiment data captured successfully |

futures_stale | bool | Futures data older than 2× TTL (>600s) |

futures_contract_exists | bool | Asset has a USDT-M perpetual contract |

futures_contract_check_failed | bool | Contract lookup failed (API error) |

mom_fallback | bool | Momentum score used fallback calculation |

vol_fallback | bool | Volatility score used fallback calculation |

spread_fallback | bool | Spread score used fallback calculation |

compression_enabled | bool | Volatility compression detection active |

pair_bonus_applied | float | Score bonus applied (0.0–5.0) |

spot_data_ok AND twitter_data_ok AND NOT futures_stale),

study data quality patterns, or use flag distributions as features.

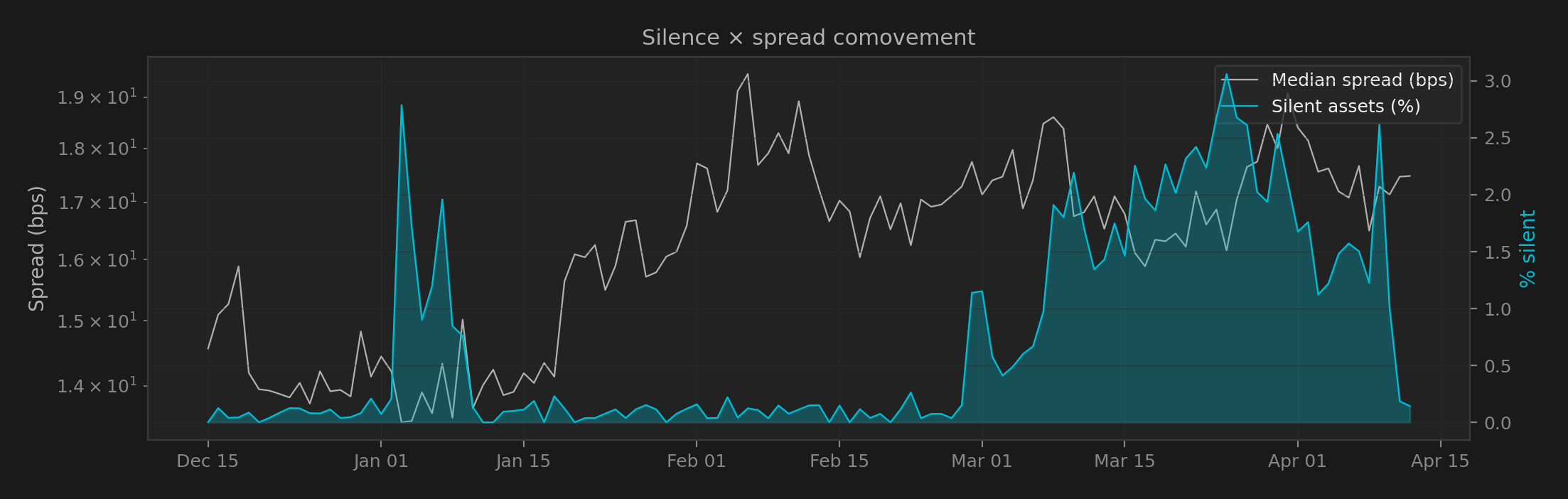

No silent data failures - if something went wrong, a flag tells you.The flag time-series

chart above shows that spot_data_ok and twitter_data_ok remain

at or near 100% across the full 80-day run.

10 Statistical Properties

We conducted a systematic statistical study across all Tier 3 features against measured returns at 1-, 3-, 6-, and 12-cycle horizons. The methodology included baseline regressions, conditioned searches, and a full-feature sweep across 4,992 statistical tests with Benjamini-Hochberg FDR correction.

Unconditional sentiment relationships

Simple sentiment-to-price relationships showed no statistical significance across all horizons tested. Hybrid mean score, AI sentiment mean, lexicon score, post volume, and positive/negative ratios all returned p-values > 0.05 when tested unconditionally against subsequent measured returns.

Observed direction was consistently contrarian: elevated sentiment preceded lower measured returns. Effect sizes were modest (25–37 basis points over 24 hours).

This suggests sentiment may function as a contrarian signal under certain liquidity conditions - a hypothesis requiring out-of-sample validation.

Derivatives and microstructure

The strongest statistical associations were observed in derivatives positioning and market microstructure features:

- Open interest flow: 5-minute OI deltas showed consistent associations with subsequent returns across multiple horizons

- Funding rates: Extreme funding (both positive and negative) preceded mean-reverting behavior

- Futures basis: Spot-futures divergence showed predictable convergence patterns

- Order book imbalance: Depth-weighted OBI at 5bps bands associated with short-horizon drift

These are well-documented market microstructure phenomena. The dataset captures them cleanly because all features share observation windows - no timestamp alignment required.

Treat these as descriptive statistics about the dataset's structure, not as evidence of exploitable patterns. Past statistical associations do not guarantee future replicability.

Full methodology: instrumetriq.com/research

11 Data Source Notes

Quote currency

Spot market data is sourced from Binance USDC pairs. Futures data is

sourced from USDT-margined perpetual contracts. Prices are functionally

identical across quote currencies (both USD stablecoins, <0.02%

difference). Order book depth and spread metrics reflect the USDC spot

market. The symbol column stores the base asset only.

Full explanation in methodology documentation.

Methodology versions

V1 (Dec 2025 – Feb 2026) used single-model DistilBERT. V2 (Feb 2026 – present) uses dual-model BERTweet + DistilBERT with crypto relevance filtering. Every row is tagged with its methodology regime.

Coverage

Binance-listed USDC spot pairs + USDT-M perpetual futures. ~275 assets as of current date. Assets are added/removed automatically as Binance listings change.